Introduction

Saving money is the backbone of creating strong financial muscle. It’s never been easier to save money in Kenya than it is today, thanks to the plethora of investment and savings platforms on the market.

If you are looking for the best money-saving apps in Kenya, you have two distinct choices:

- Wealth-Building Apps: Apps that hold your money and pay you interest (like Cashlet or Zimele).

- Wealth-Finding Apps: Apps that track your M-Pesa automatically to stop your financial leaks, so you actually have money to save at the end of the month.

You need both. In this guide, we break down the top 5 apps in Kenya to help you manage expenses, earn interest, and secure your financial future.

The 5 Best Apps for Saving Money in Kenya

Here are five leading apps designed to help Kenyans manage, save, and grow their money more effectively:

1. Kiihela

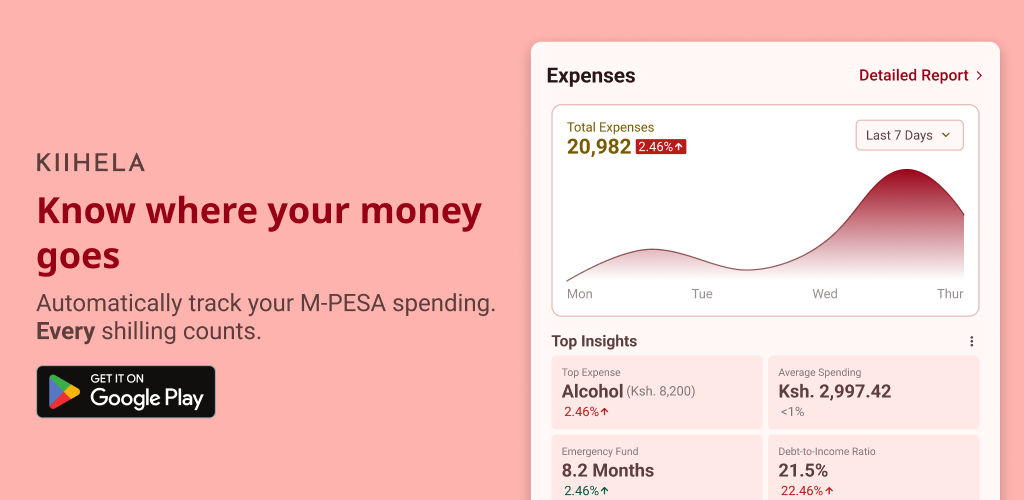

Before you can earn interest on your savings, you actually need money to save.

Most Kenyans fail at saving not because they don’t want to, but because they suffer from “M-Pesa leaks”—small daily expenses that drain their accounts unnoticed.

Kiihela is a smart financial assistant that solves this. It doesn’t hold your savings; it finds the money you didn’t know you had by automatically tracking your M-Pesa income and expenses.

Key Features:

- M-Pesa Integration: Securely connects to your M-Pesa account to automatically fetch and categorize transactions, providing a real-time view of your spending without manual entry.

- Expense & Income Tracking: Automatically categorizes transactions, allowing you to see exactly where your money goes (e.g., transport, food, bills).

- Budgeting Tools: Allows users to create custom budgets for different categories (e.g., groceries, entertainment) and track spending against these limits.

- Goal Setting: You can set financial goals (e.g., save for a phone, emergency fund), but Kiihela primarily tracks your progress based on your overall financial health rather than holding dedicated funds.

Download Kiihela on the Google Play Store today.

2. Cashlet

Overview:

Cashlet provides a streamlined mobile platform giving users access to a diverse range of savings and investment products from multiple established fund managers in Kenya. It acts as a convenient gateway to easily compare and invest in different types of funds.

Key Features

- Offers access to 8+ different savings and investment products, including Money Market Funds (MMFs), Fixed Income Funds, USD Funds, and Shariah-compliant Funds, and features products from fund managers such as ICEA Lion Asset Management, Etica Capital, Nabo Capital, and Orient Asset Managers, with more potentially added over time.

- Highly accessible, with a minimum investment amount of Ksh. 50.

- Enables users to create financial goals and monitor investment growth in real-time.

- Instant withdrawal for amounts under Ksh. 10,000. Amounts above that are processed in 3 working days.

- A true lock savings option for disciplined saving. You cannot withdraw money under any circumstances until the maturity date.

- Interest is calculated daily and credited to the user’s Cashlet account daily around 10 am.

Fees

- Fund Manager Fees: The primary cost is the annual management fee charged by the respective fund manager (e.g., ICEA Lion, Etica), typically ranging from 1% to 2.5% p.a., deducted from the fund’s overall returns. This is standard for Unit Trusts.

- Cashlet Platform Fees: Cashlet also charges a withdrawal fee depending on the amount withdrawn.

Security & Regulation

- Cashlet states it is regulated by the Capital Markets Authority (CMA). Users should verify this status independently on the CMA website.

- Funds are invested in market instruments and are not insured by KDIC.

3. Chumz

Overview

Chumz aims to make saving easy and accessible, particularly for young people or first-time savers. It cleverly integrates goal-setting with micro-investment, channeling saved funds into an underlying investment product ( typically a Money Market Fund via a regulated partner) to help your money grow.

Key Features

- Goal Creation: Users set specific, tangible savings goals (e.g., “New Phone Fund,” “Rent Deposit”), making saving purposeful.

- Flexible Saving Methods: Offers various ways to save, including automated recurring deposits (daily, weekly, monthly) and manual top-ups via M-Pesa.

- Underlying Investment: Savings are channeled into a Money Market Fund managed by a partner firm (Nabo Capital is a known partner). This allows savings to earn potential returns based on MMF performance.

- Interest Rates/Returns: Returns are derived from the performance of the partner MMF (e.g., Nabo Capital MMF). Expect variable returns historically in the 8-12% p.a. range (gross), but this is not guaranteed and fluctuates with market conditions. Interest is typically calculated daily and compounded monthly. The net return will be after the fund manager’s standard annual management fee is deducted.

Fees:

Chumz has a transparent fee structure:

- Deposits: No fees charged by Chumz. Users only incur the standard M-Pesa Paybill charges levied by the mobile service provider (Safaricom).

- Withdrawals: Chumz charges a small, flat withdrawal fee to cover operational costs:

- KES 20 for withdrawing amounts less than KES 1,000.

- KES 30 for withdrawing amounts from KES 1,000 up to KES 150,000 (standard M-Pesa transaction limits apply).

- Underlying Fund Management Fee: This is separate from Chumz’s fees. The partner fund manager (e.g., Nabo Capital) charges an annual management fee (typically 1-2.5% p.a.) which is deducted directly from the fund’s overall returns before they are distributed to investors. This is standard practice for all Unit Trusts.

Security & Regulation

Uses encryption for data protection. The partner fund manager (e.g., Nabo Capital) is licensed and regulated by the Capital Markets Authority (CMA). User funds are invested through this regulated entity, providing oversight. Funds are invested in the market and are not covered by KDIC.

4. Zimele

Overview:

Zimele Asset Management is a long-established fund manager (since 1998), licensed by the Capital Markets Authority (CMA). Their platform (accessible via Web and a dedicated Android App) provides Kenyans direct access to invest in their own range of Unit Trust funds, offering options for both saving and long-term investment.

Key Features

- Zimele offers two main funds: the Zimele Savings Plan (Money Market Fund) invests in low-risk, interest-earning assets like Treasury bills/bonds. While the Zimele Investment Plan (Balanced Fund) invests in a mix of shares listed on the Nairobi Securities Exchange (NSE) and interest-earning assets.

- Low Minimum Investment: Start investing in either fund with just KES 100.

- Accessibility: Manage investments via the Zimele website or the Android mobile app. Deposits can be made easily via M-Pesa Paybill, cheque, or standing order.

- Account Types: Supports individual, joint, chama, group, and corporate accounts.

- Transparency: Provides online statements and performance tracking via web/app. Fund performance is also often published in national newspapers.

Interest Rates/Returns:

- Money Market Fund: Offers variable interest based on the performance of underlying fixed-income assets. Zimele describes it as “competitive.” Crucially, interest is compounded annually, which is less frequent than many other MMFs that compound monthly or daily. Returns are not guaranteed.

- Balanced Fund: Returns are primarily through potential capital gains on the units, driven by stock market performance and interest income. Designed for long-term growth (2+ years recommended), performance can be volatile, and returns are not guaranteed.

Fees

The Zimele Savings Plan (MMF): Subject to an annual management fee of 2% of the funds under management. The brochure states “no hidden charges” for this fund beyond the management fee (standard M-Pesa deposit charges apply).

However, the Zimele Investment Plan (Balanced Fund): Has a more complex fee structure:

- Initial Administration Fee: 3% charged on every new investment/deposit made into the fund. *j Annual Management Fee: 2.5% of the funds under management.

Security & Regulation:

Zimele Asset Management Ltd is licensed and regulated as a fund manager by the CMA. It employs the structure mandated for Unit Trusts:

- Custodian: Standard Chartered Securities Services holds all client assets (cash and investments) safely, separate from Zimele’s own accounts.

- Trustee: Kenya Commercial Bank (KCB) Trustee Services ensures Zimele acts in the best interest of investors according to regulations.

This separation significantly enhances security and reduces operational risk. Investments themselves carry market risk and are not covered by KDIC.

Disclaimer

Information provided here, especially regarding interest rates, fees, and specific partners, is based on general knowledge and typical structures. These details can change.

Always verify the latest information directly from the app providers’ official websites, terms of service, and relevant regulatory bodies (CMA, CBK) before making any financial decisions.

This article is for informational purposes only and does not constitute financial advice. Remember that investments carry risk, and past performance is not indicative of future results.